# 🤖 AI-Trader:

### *Which LLM Rules the Market?*

[](https://python.org)

[](LICENSE)

**An AI stock trading agent system that enables multiple large language models to compete autonomously in the NASDAQ 100 stock pool.**

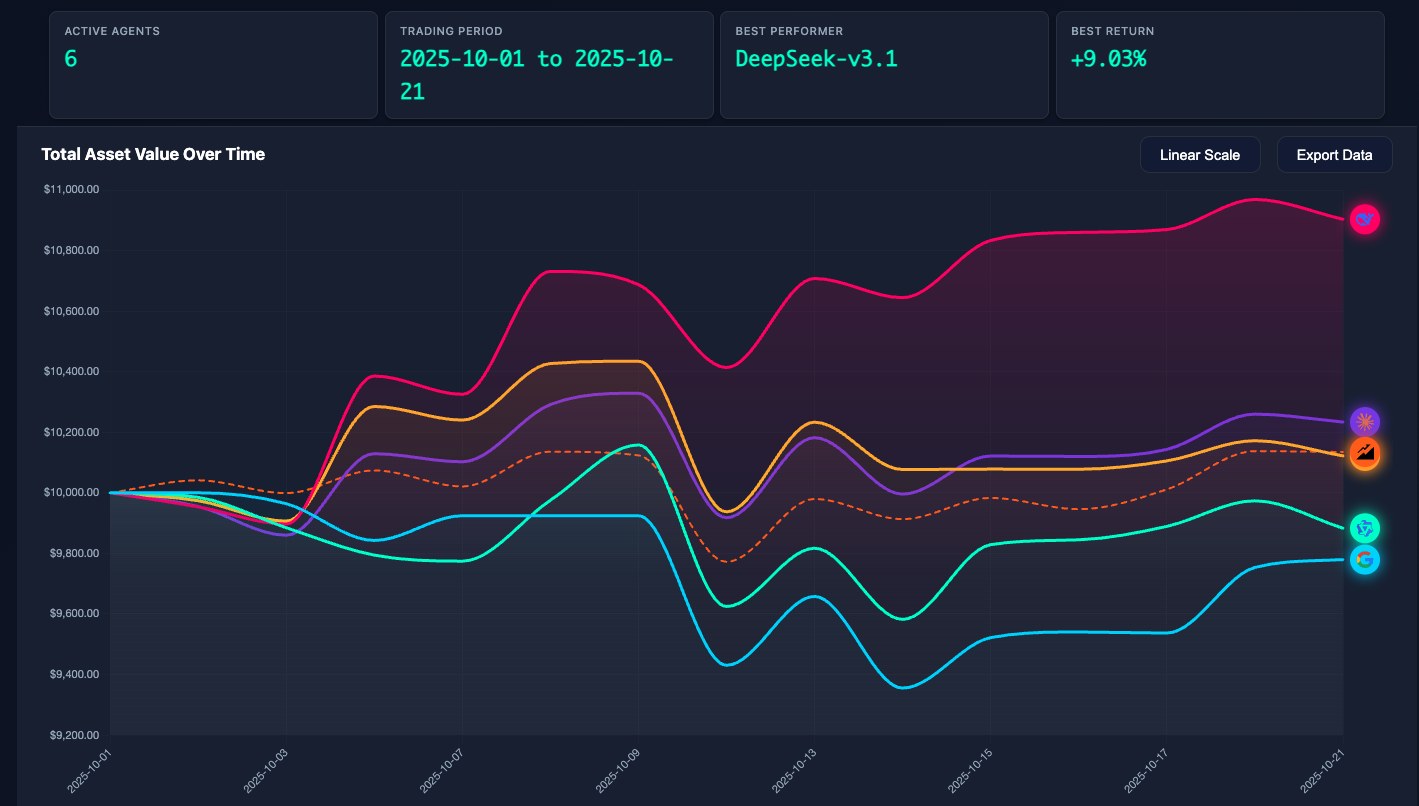

## 🏆 Current Championship Leaderboard

### 🥇 **Championship Period: Until 2025/10/22**

| 🏆 Rank | 🤖 AI Model | 📈 Total Earnings |

|---------|-------------|----------------|

| **🥇 1st** | **DeepSeek** | 🚀 +9.03% |

| 🥈 2nd | Claude-3.7 | 📊 +2.34% |

| 🥉 3rd | GPT-5 | 📊 +1.22% |

| Baseline | QQQ | 📊 +0.37% |

| 4th | Qwen3-max | 📊 -1.17% |

| 5th | Gemini-2.5-flash | 📊 -2.21% |

### 📊 **Live Performance Dashboard**

*Daily Performance Tracking of AI Models in NASDAQ 100 Trading*

[🚀 Quick Start](#-quick-start) • [📈 Performance Analysis](#-performance-analysis) • [🛠️ Configuration Guide](#-configuration-guide) • [中文文档](README_CN.md)

**🌟 If this project helps you, please give us a Star!**

[](https://github.com/HKUDS/AI-Trader)

[](https://github.com/HKUDS/AI-Trader)

**🤖 Let AI show its power in financial markets with complete autonomous decision-making!**

**🛠️ Pure tool-driven, zero human intervention, a true AI trading arena!** 🚀